In This Issue ![]()

| Last Week in Review: Rumors were swirling out of Europe, while inflation news was swirling here at home.

Forecast for the Week: The second half of the week heats up with news on the housing market and the state of the economy. Plus, the Fed meets. View: A fee increase is coming that will impact home loan rates. Be sure to read the details below. |

| Last Week in Review |

It’s almost all Greek to me. Last week, more news from Greece hit the wires, as did several pieces of inflation news here at home. Read on to learn what happened, and what the impact was on home loan rates.

First, it’s important to remember that back in October, a deal called for Bondholders to “accept” a 50% haircut on the face value of the Greek debt. Last week, rumors about this amount were swirling, saying that Greece is close to a deal that would entail a 68% haircut on the face value of their debt. And if that’s not concern enough, a larger issue remains. First, it’s important to remember that back in October, a deal called for Bondholders to “accept” a 50% haircut on the face value of the Greek debt. Last week, rumors about this amount were swirling, saying that Greece is close to a deal that would entail a 68% haircut on the face value of their debt. And if that’s not concern enough, a larger issue remains.After the proposed austerity measures, wage cuts, and tax increases are instituted, will Greece – not to mention Italy, Portugal, and other struggling economies – be able to “grow” their way out of debt? Given that the World Bank lowered its 2012 global growth forecast to 2.5% from last summer’s estimate of 3.6%, the odds sure seem tough. This is an important story to watch as the year unfolds. Here at home, inflation was in the news twice last week…and the results were mixed. On Wednesday, the wholesale inflation measuring Core Producer Price Index (PPI) came in hot, elevating the year-over-year Core PPI rate to a lofty 3%…the highest since April 2009. Meanwhile, Thursday’s Core Consumer Price Index (CPI) was inline with expectations and tame overall, though it is worth noting that the 2.2% Core CPI year-over-year reading is near the upper end of the Fed’s tolerance level. Remember, inflation is the archenemy of Bonds and home loan rates, like Kryptonite to Superman. That’s because inflation erodes the value of the fixed return provided by a Bond, which causes home loan rates to rise. It will be interesting to see what – if anything – the Fed says about inflation after it’s regularly scheduled meeting of the Federal Open Market Committee this week…as any talk or sign of inflation can move the markets and impact rates. Even with all the news last week, it’s still a great time to purchase or refinance a home. Let me know if I can answer any questions at all for you or your clients. |

| Forecast for the Week |

|

The reports that will be released this week will carry some weight:

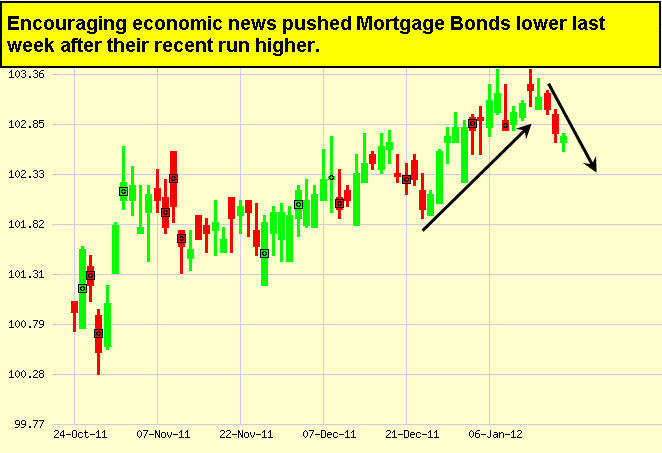

In addition to those reports, the Federal Open Market Committee will hold a two-day meeting this week. The meeting will begin January 24 and end with a policy statement at 12:30 pm ET on January 25. There is no chance of a rate hike, but I will be listening for any hint of a third round of Quantitative Easing (QE3). Remember: Weak economic news normally causes money to flow out of Stocks and into Bonds, helping Bonds and home loan rates improve, while strong economic news normally has the opposite result. As you can see in the chart below, some encouraging economic and company earnings news last week helped halt the improving trend Bonds had been seeing. I’ll continue to monitor this situation. Chart: Fannie Mae 3.5% Mortgage Bond (Friday Jan 20, 2012)

|

| The Mortgage Market Guide View… |

| Fee Increase to Impact Home Loans

In December 2011, Congress reached a last-minute deal to fund the payroll tax cut extension. The payroll tax extension will provide a 2% tax reduction for individuals making up to $106,800, so the tax extension will be very helpful for many Americans who are struggling during these tough economic times. But like so many things in our tangled economy, there’s a flip side. In this case, the tax cut deal has a rippling effect that will impact the mortgage world. Here’s what’s happening and what it means to home loan rates: What is happening and why? To put it bluntly, the passage of the payroll tax cut extension is being funded via a mandate to Fannie Mae and Freddie Mac (the nation’s largest providers of mortgage money) to increase their guarantee fees or “g-fee’s” by at least 10 basis points on the rate. So rather than giving a par rate of 4.00%, for example, the par rate is now increased by at least 10 basis points, or approximately 4.10%. But as you probably know…home loan rates are priced and offered in .125% increments, so this will most likely impact the consumer by .125% in rate. Whether you agree or not on the politics behind this cost being passed along to folks who are taking out mortgages, the Congressional Budget Office recently estimated that the increase will ultimately pay for about $35.7 Billion of the cost of the payroll tax extension. What exactly is this “g-fee”? The guarantee fee or “g-fee” is an amount charged by mortgage-backed securities (MBS) providers, like Freddie Mac and Fannie Mae, to help protect against credit-related losses in the overall mortgage portfolio. In other words, it acts a lot like insurance and helps lower the overall risk…which means home loans can be offered at terrific interest rates to borrowers that have good – but not perfect – credit. What exactly is the impact of the rate increase? For example, for a $200,000 home loan, the increased g-fee (assuming a .125% increase in rate) would equate to $250 more per year in interest, or $7,500 more over 30 years. Someone buying or refinancing a home can certainly choose to buy down the cost with cash up front – but most folks will not do this. Who will this impact? The change will impact all new borrowers of Fannie Mae and Freddie Mac loans. The bill will also impact Federal Housing Administration (FHA) loans by increasing the annual mortgage insurance premium that borrowers pay by one-tenth of a percent. When will it start? Officially, the increase to guarantee fees will begin on April 1, 2012. However, the increase is already starting to be seen in rate sheets right now, since home loans being originated now will likely not be closed, pooled and securitized until April…and therefore will need the increased g-fee priced in earlier. How long will this be in effect? The increase will be effective through October 1, 2021. The bottom line is that the g-fees will be going up…and this will impact homebuyers looking to obtain a home loan through Fannie Mae, Freddie Mac and FHA. The good news is that home loan rates are still at historic lows right now, and it’s a great time to purchase a new home or refinance. If you or anyone you know has any questions, please call or email! Economic Calendar for the Week of January 23 – January 27

|

|

The material contained in this newsletter is provided by a third party to real estate, financial services and other professionals only for their use and the use of their clients. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, we do not make any representations as to its accuracy or completeness and as a result, there is no guarantee it is without errors.

|